Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios. Wednesday: • At 7:00 AM ET, The Mortgage Bankers As...

Why it matters

- The current mortgage rates can greatly influence home buying decisions, impacting the housing market's overall health.

- Fluctuations in mortgage rates reflect broader economic trends, providing insights into future financial conditions.

- Understanding these rates can help potential homeowners make informed financial choices.

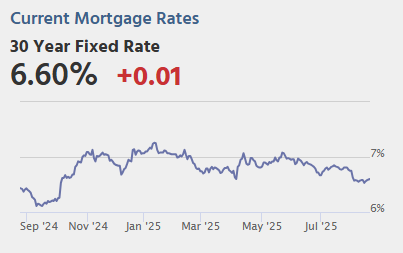

On Wednesday, mortgage rates continue to show variability, a trend that is essential for both potential homebuyers and the broader economy. According to data sourced from MortgageNewsDaily.com, these rates are particularly relevant for top-tier scenarios, indicating a benchmark for those seeking the most favorable borrowing conditions. The dynamics of mortgage rates are influenced by a myriad of factors, including inflation, Federal Reserve policies, and overall economic performance.

Recent reports suggest that the mortgage market remains sensitive to shifts in economic indicators. With inflation rates remaining a focal point for policymakers, mortgage rates are expected to reflect these changes closely. As the Federal Reserve contemplates its next moves regarding interest rates, mortgage rates could further fluctuate, impacting affordability for prospective homeowners.

In the current landscape, buyers are advised to stay informed about these changes. Higher mortgage rates can lead to increased monthly payments, which can deter potential buyers and slow down the housing market. Conversely, lower rates could spur demand, leading to a more competitive market.

In recent weeks, the Mortgage Bankers Association (MBA) has reported on these trends, outlining how shifts in interest rates are affecting loan applications. The association's updates highlight that while some buyers are waiting for more favorable rates, others are moving forward with purchases, recognizing that waiting may not always yield better conditions.

The housing market's reaction to mortgage rate changes is equally critical. Recent analysis shows that as rates rise, the number of applications for home loans tends to decrease. This drop in applications can signal a cooling of the housing market, which has seen significant price increases in the past few years. Conversely, as rates stabilize or decrease, there is often a resurgence in applications as buyers re-enter the market, eager to capitalize on better financing options.

Moreover, the current mortgage landscape is shaped not just by domestic factors but also by global economic conditions. Investors worldwide are monitoring U.S. economic indicators, which can impact international borrowing costs and ultimately influence mortgage rates domestically. This interconnectedness emphasizes the importance of understanding the broader economic context when evaluating mortgage options.

As we delve deeper into the specifics of mortgage rates, it is crucial to acknowledge that they are not uniform across different types of loans or borrower profiles. Individuals with higher credit scores and stable financial backgrounds typically secure lower rates, while those with less favorable credit histories may face higher borrowing costs. This disparity highlights the need for potential buyers to assess their financial situations and explore ways to improve their creditworthiness before applying for a mortgage.

In light of these developments, prospective buyers are encouraged to remain proactive. Engaging with financial advisors or mortgage professionals can provide valuable insights tailored to individual circumstances. Additionally, comparing various mortgage products and understanding the fine print can lead to more informed decisions.

In summary, the current state of mortgage rates is a reflection of a complex interplay between local and global economic factors. With ongoing fluctuations, it is essential for buyers to stay updated and prepared for various scenarios. The decisions made today regarding mortgage applications and purchases will have lasting implications for both individual finances and the housing market as a whole.